Breaking up with your legacy card provider

The corporate card is probably the longest active relationship in your finance stack, and the one you've thought least about. Someone else set it up, on terms from a different era, and the questioning stopped years ago.

It might have felt like love the day those first three shiny cards arrived. But the case for parting ways has been building. Cloud spend is bigger than ever, headcount is more distributed, and accounting setups are more complex. Meanwhile, the classic corporate card, the instrument carrying a large share of your operating spend, hasn't meaningfully changed since the early 2010s. It's the last part of your finance stack still operating like it's pre-broadband.

This piece is about the moment that becomes obvious. The symptoms you've been ignoring. And what the alternative looks like once you're ready to explore the market again.

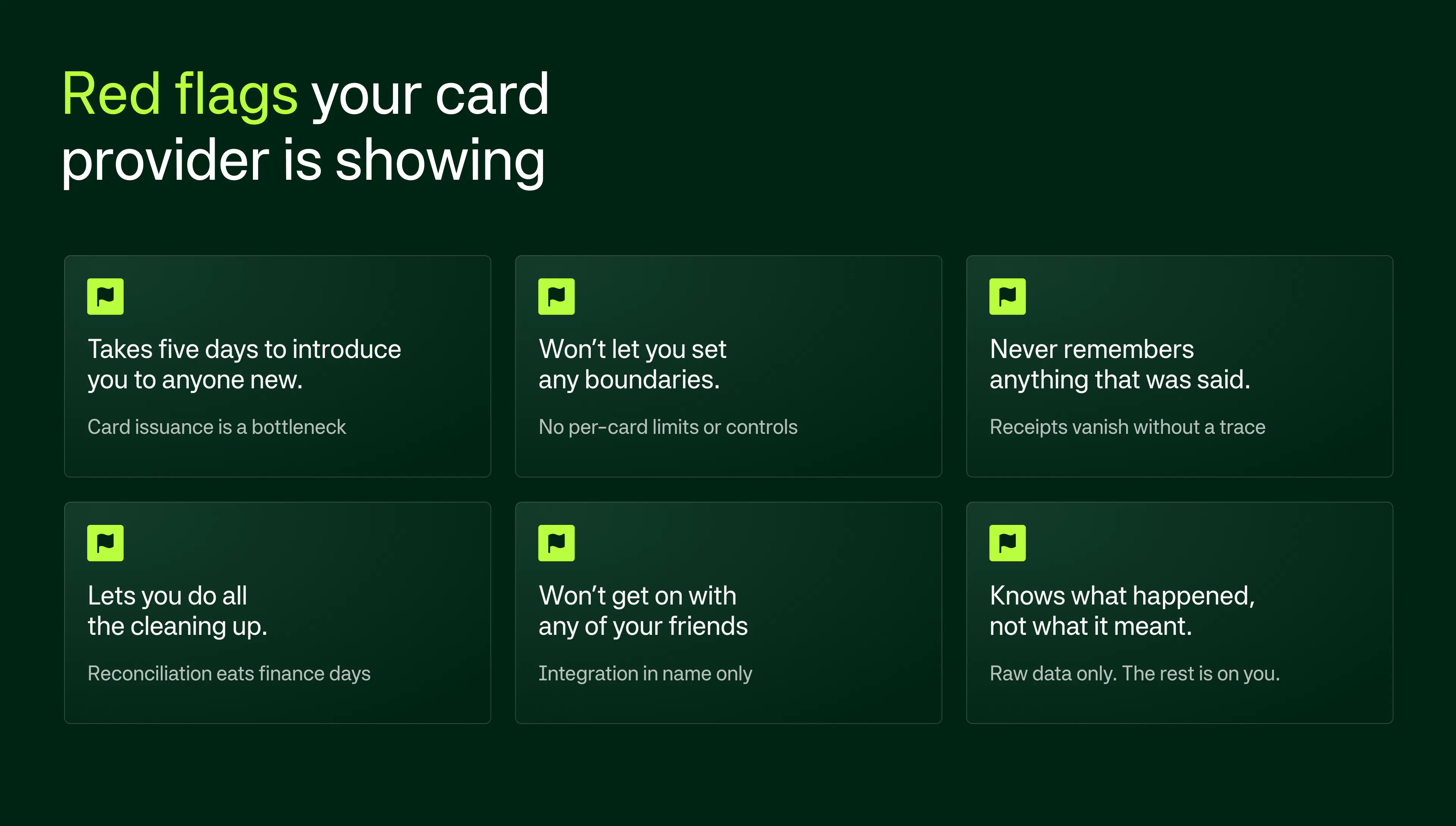

The signs you've outgrown your legacy card

You don't usually wake up convinced your card provider is the problem. Like most fading relationships, it's the cumulative weight of many small betrayals:

- You issue fewer cards than you should. Every new card requires a phone call, a paper form, a five-day wait, and a fee for the privilege. So you don't bother, and two senior people end up paying for everything.

- You can't set meaningful controls. Per-card limits, vendor locks, merchant restrictions, recurring SaaS caps. They’re all off limits, which means you either don't issue cards to people who'd benefit, or you do and hope for the best.

- Receipts are a black hole. Finance spends every month chasing the same people, three levels above them, with apologetic Slack messages.

- Reconciliation eats two to four days a month, per finance person. Annualised, that's a hire's worth of work burned on the lowest form of finance.

- The 'integration' is a CSV download. Most legacy cards don't really sync, they hand you a CSV download. Even the more sophisticated providers that do sync into Xero, QuickBooks, or DATEV stop at the transaction itself: no receipts, no VAT codes, no cost centres. Your team hand-codes the rest.

- Reporting is a screenshot of a screenshot. The dashboard doesn't know which team owns which card, or which vendors count as 'paid social'. Any real question gets answered in Excel, after month-end, once the coding is finally done.

Why this is more expensive than it looks

Most legacy cards grew up around a different core business: lending, credit, and interchange. The card was the original product, and the spend software was layered on later. That history shows up in predictable places. Manual work compounds, and your team subsidises it with their evenings. Reporting lags reality, so you're always answering last month's questions. And the pain scales with the business, meaning what worked at 30 employees breaks at 200.

The proof tends to land hard once people switch to a modern spend management solution. Case in point:

Venture Beyond reclaimed £30k in VAT after moving to Moss. SNOCKS cut their month-end by 70%. Hive runs entities across six countries on a single platform, and cut invoice processing by 75% along the way.

The excuses for staying

"We're tied in until October." Contractual inertia usually looks more binding than it is, particularly outside of bespoke commercial deals. The relationship manager has every incentive to keep you in the relationship. But the annualised cost of staying almost always exceeds the cost of breaking early.

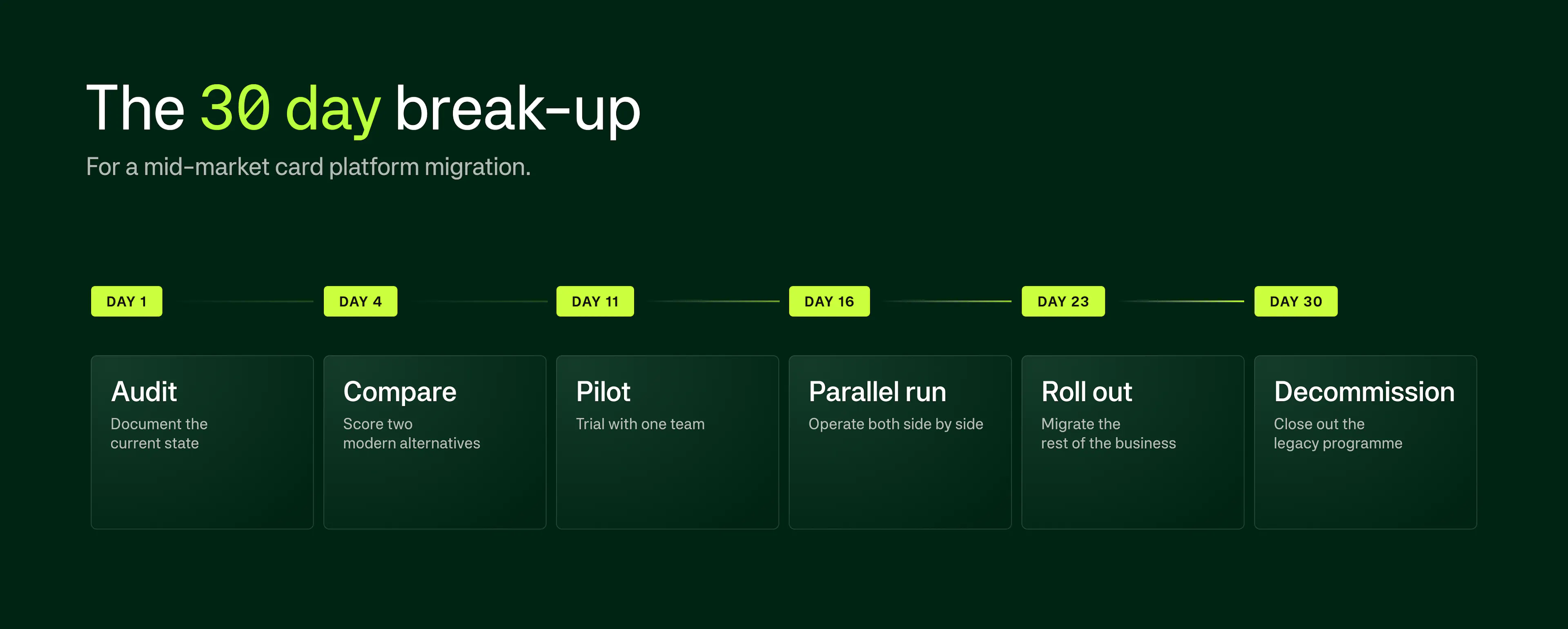

"I don't have bandwidth for a six-month migration." Fair, but that's not what this looks like. You're thinking of ERP, with steering committees and parallel-run periods. A mid-market card migration takes weeks.

"We've been together for fifteen years." Switching cards somehow feels disloyal in a way that switching your data warehouse never would. But it isn't. The card should earn its place like every other vendor in the stack. And if you're worried about the banking relationship, you can usually keep that and unbundle the card.

What modern actually means

A spend platform worth switching to should give you, at a minimum: limits that flex with the business rather than a one-size-fits-all cap, workflow applied at the moment of transaction so finance handles exceptions instead of doing month-end data entry, real bidirectional sync into Xero, DATEV, NetSuite, Sage and the rest with receipts and tax codes preserved end to end, mid-month reporting you can actually use, and virtual cards issued in seconds with per-card limits and vendor locks.

The shift from retrospective to real-time is the biggest operational gain most teams describe after migrating.

The breakup is shorter than you think

The biggest blocker to switching isn't the technology. It's the assumption that switching is a project. At mid-market scale, 30 days is realistic: a few days to audit cardholders and spend, a week to compare alternatives, a pilot with one team where card spend is highest, a brief parallel run, rollout, decommission. Bigger businesses need more orchestration, but the shape doesn't change.

Your AP system, payroll, CRM, data warehouse: none of these are forever decisions. They get re-evaluated, and when something better shows up, they get replaced. The corporate card has been strangely exempt from that scrutiny for a long time.

If your legacy cards are making your finance team slower, your reporting blurrier, and your month-end longer, your team deserves better. There weren't good options fifteen years ago, but now there are.

Ready to start seeing other cards? Get in touch with our team for a first look at the Moss platform.